Glossary of Credit Limit Model Terms

User-Supplied Inputs to the Credit Limit Model

Expected Monthly Sales -

The average amount you expect to sell to this customer on a monthly basis. It can also be a seasonal amount.

Months Outstanding Allowed (DSO) -

The sales balance limit (or DSO) imposes an upper bound on your cash exposure to the customer, based on the amount of your sales to the customer and the maximum time-to-pay you will tolerate. As an example, if the sales terms for this customer are 15 days and your maximum delinquency tolerance is 30 days, then enter 1.5 months (30 + 15 = 45 days or 1.5 months). The minimum value that can be entered is 1.

Expected-loss Limit -

Best practices require annual budgeting for write-offs at the credit portfolio level. This write-off budget is your company's "expected credit loss" for the fiscal year. Setting a credit limit requires that you allocate a portion of this "expected credit loss" budget to an individual customer. The model combines your input of this budget with the customer's probability of default, to calculate a credit limit that controls your write-offs.

For example, if your annual budget for write-offs is $500,000 on annual sales base of $50 million, that's 1%. So, the expected loss for a $100,000 relationship would be $1,000 at the same 1% rate. On a statistical basis, this will control your write-offs to 1%.

Risk Appetite -

Select the level of risk that is consistent with your credit strategy. Select "Aggressive" if your company/division follows an aggressive credit strategy. Companies entering new markets often accept higher risk to build market share quickly. Select "Conservative" if your company/division follows a conservative credit strategy. Companies with unique products and minimal competitive market pressures often follow a conservative credit policy. Select "Middle" if your company/division follows a neutral credit policy, (between Aggressive and Conservative). You have the option of setting the risk appetite at the customer or portfolio level.

Cost of Capital -

Your company's cost of capital expressed as a percent.

Gross Profit Margin -

Your expected gross profit margin on sales to this customer expressed as a percent. If you do not forecast gross profit margins on a customer-by-customer basis you can use your company's overall budgeted margin.

Existing Credit Limit -

Your current credit limit for this customer. Typically the credit limit represents that maximum exposure, at any one point in time, which you are willing to accept from the customer.

Monitor Credit Limit -

Monitoring the maximum credit limit is simple. To activate the monitoring service:

- Check the box next to "Monitor Credit Limit."

- Set a high monitor value (upper box), which will alert you if our maximum goes ABOVE this amount (possible opportunity to sell more).

- Set a low monitor value (lower box), which alerts you if our maximum falls BELOW that amount

- Click "Calculate Credit Limit"

Limits will be automatically calculated nightly and compared to your threshold range.

The credit limit calculated for your customer may fall.

If it falls below your low monitor value, you may want cut the customer's credit line or take other action.

You can also re-set the monitor, to warn you if things continue to get worse.

Any email alerts are sent daily, and contain supporting detail with highlights and links to our fundamental service, so you can quickly determine what to do.

And of course a high monitor alert can indicate an opportunity for you to increase a credit line.

Alert summaries are available on the "My Current News" page.

Top

Credit Limit Model Results

The model actually calculates three separate limits using three different methods.

The model is set to be conservative and therefore the highest limit is discarded.

The lowest computed limit becomes your recommended limit, and the other becomes the maximum.

Maximum Credit Limit -

The maximum credit limit recommended for this customer. This limit will be the base used for monitoring the customer's credit limit, if you choose to use the monitoring feature.

Recommended Credit Limit -

The credit limit recommended for a customer is typically based on your expected monthly sales and months outstanding allowed.

Existing Credit Limit -

Your current credit limit for the customer. Typically the credit limit represents that maximum exposure, at any one point in time, which you are willing to accept from the customer.

Opportunity -

The additional credit limit capacity available based on the difference between the recommended credit limit and the existing credit limit.

- OR -

Gap -

The shortfall in the recommended credit limit versus the existing credit limit.

Moody's Rating -

See Moody's Rating Terms.

S&P Rating -

See Standard and Poor's Rating Terms.

Altman's Z" score -

See Z"-score in the glossary of financial terms.

Stock Volatility -

A measure of the amount by which a company's daily stock price fluctuates over a trailing 6 month period, with greater weighting given to the recent months.

The Merton Model uses volatility to provide a daily estimate of credit risk. It leverages marketplace knowledge to achieve predictive accuracy beyond what can be done with financial statements alone. Volatility is typically a value between 0 and 1. A LOWER VALUE IS BETTER.

Leverage -

A calculation of Leverage & Debt Coverage. Leverage is Total Liabilities divided by Total Assets, and is typically between 0 and 1.4. A LOWER VALUE IS BETTER.

FRISK® Score -

See FRISK® score in the glossary of financial terms.

Financials Date -

The date of the financials used in the credit limit calculations.

Top

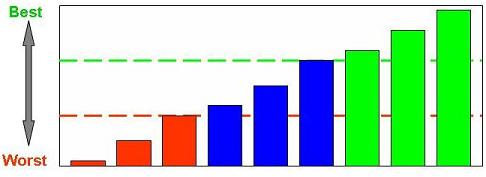

Credit Limit Influences

Small red bars are the worst and tall green bars are the best. Blue bars note intermediate values.

The following shows the progression of the bars from worst (small red) to best (tall green).

Up to four bars may be shown depending on the amount of data/ratings available to the model for determining Moody's or Fitch Ratings, Z" Score, Stock Volatility and Leverage. More bars mean you can attach a higher weight to the model's recommendation.

Hint - Clicking on the chart bars will give you more details to focus your analysis to save you time.

Copyright © 2026 by CreditRiskMonitor.com (Ticker: CRMZ®).

All rights reserved.

Reproduction not allowed without express permission by CreditRiskMonitor.

The information published above has been obtained from sources CreditRiskMonitor considers to be reliable.

CreditRiskMonitor and its third-party suppliers do not guarantee the accuracy and completeness of the information and specifically do not assume responsibility for not reporting any information omitted or withheld.

The FRISK® scores, agency ratings, credit limit recommendations and other scores, analysis and commentary are opinions of CreditRiskMonitor and/or its suppliers, not statements of fact, and should be one of several factors in making credit decisions.

No warranties of results to be obtained, merchantability or fitness for a particular purpose are made concerning the CreditRiskMonitor Service.

By using this website, you accept the Terms of Use Agreement.

Contact Us: 845.230.3000

Fundamental financial data concerning public companies may be provided by LSEG Data & Analytics (click for restrictions)

Thursday, April 30, 2026

|

|